If you run a small business in India — an electrical shop, a kirana store, a wholesale outlet, or any retail business — there is one thing that silently drains your revenue every single month.

Unpaid credit. Udhar.

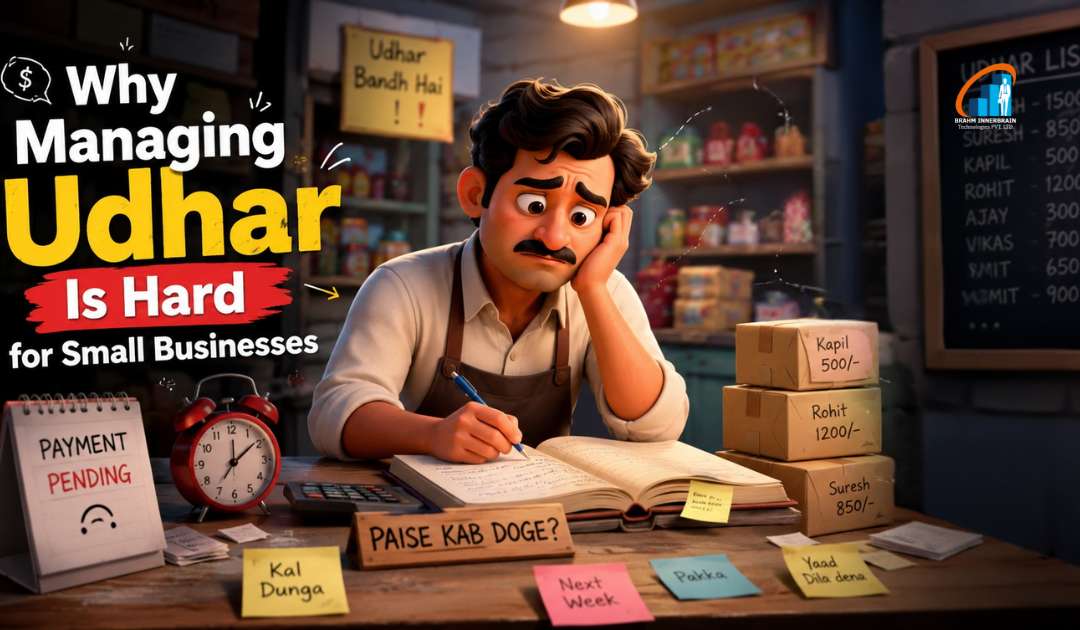

“Bhaiya, will pay tomorrow.”

“Next month for sure.”

“Don’t have change right now.”

These seem like small, harmless conversations in the moment. But when 10 to 20 customers have outstanding amounts and the total quietly crosses ₹20,000 to ₹30,000 — with no clear record of who owes what — you realize just how serious this problem really is.

In this article, we break down why managing credit (udhar) is so difficult for small business owners, and walk you through a practical, digital solution that thousands of Indian businesses are already using.

The Real Problem With Udhar — It’s Not Just “People Don’t Pay”

Most business owners think the problem is simply that customers don’t pay on time. But the real problem starts much earlier — with poor tracking.1. No Proper Records

Most small shopkeepers still rely on a handwritten register to track credit. And that register:

- Gets misplaced or lost

- Gets damaged by water or wear

- Has unclear, overwritten entries

- Can only be read by the person who wrote it

When the record itself is unreliable, how do you confidently know whether Ramesh bhai paid ₹500 last week or not?

2. Sending Reminders Feels Awkward

This is the biggest emotional barrier small business owners face. Your customers are often neighbours, relatives, or long-time regulars. Asking for money too bluntly risks damaging the relationship. Staying silent means you never get paid.

Because of this awkwardness, many business owners delay reminders for weeks — and by then, the customer has conveniently “forgotten.”

3. You Don’t Know the Exact Total Per Customer

A single customer borrows ₹200, then ₹450, then ₹100, then ₹800, then ₹300 across five different visits. What’s the total? If everything is in a scattered register, you have to add it up every time manually. And if the customer disputes an amount, you have no solid proof.

Without accurate records, you can’t even have a confident conversation about what’s owed.

4. Cash Flow Becomes Impossible to Predict

Your monthly sales show ₹50,000 — but only ₹27,000 actually came in as cash. The remaining ₹23,000 is stuck in outstanding credit. Without knowing the exact figure at any point, how do you plan stock purchases, manage expenses, or make business decisions?

5. Old Credit Is Practically Written Off

When records aren’t maintained properly, outstanding amounts older than 3 to 4 months are essentially lost money. Both you and the customer forget. It silently becomes a business loss — one that never shows up in your books, but always shows up in your stress.

This Is Not Just Your Problem

India has over 6 crore registered small businesses, and the MSME sector consistently shows that 15 to 25 per cent of a small retailer’s revenue is tied up in outstanding credit at any given time.

That means if your monthly sales are ₹1 lakh, between ₹15,000 and ₹25,000 is always sitting outside your business — in someone else’s pocket.

This is not a personal failure. It is a systemic problem that affects millions of small business owners across India who lack the right tools to manage it.

Why Traditional Solutions Don’t Work

Many business owners try workarounds — going cash-only, keeping a stricter register, calling customers personally. These help to some extent, but:

- You cannot realistically go fully cash-only without losing customers

- Maintaining a manual list is time-consuming and error-prone

- Personal calls are awkward and don’t scale as your customer base grows

The real solution is not more discipline — it is a smarter system that tracks credit automatically, sends reminders professionally, and gives you a real-time view of your outstanding balance at all times.

3. You Don’t Know the Exact Total Per Customer

A single customer borrows ₹200, then ₹450, then ₹100, then ₹800, then ₹300 across five different visits. What’s the total? If everything is in a scattered register, you have to add it up every time manually. And if the customer disputes an amount, you have no solid proof.

Without accurate records, you can’t even have a confident conversation about what’s owed.

4. Cash Flow Becomes Impossible to Predict

Your monthly sales show ₹50,000 — but only ₹27,000 actually came in as cash. The remaining ₹23,000 is stuck in outstanding credit. Without knowing the exact figure at any point, how do you plan stock purchases, manage expenses, or make business decisions?

5. Old Credit Is Practically Written Off

When records aren’t maintained properly, outstanding amounts older than 3 to 4 months are essentially lost money. Both you and the customer forget. It silently becomes a business loss — one that never shows up in your books, but always shows up in your stress.

This Is Not Just Your Problem

India has over 6 crore registered small businesses, and the MSME sector consistently shows that 15 to 25 per cent of a small retailer’s revenue is tied up in outstanding credit at any given time.

That means if your monthly sales are ₹1 lakh, between ₹15,000 and ₹25,000 is always sitting outside your business — in someone else’s pocket.

This is not a personal failure. It is a systemic problem that affects millions of small business owners across India who lack the right tools to manage it.

Why Traditional Solutions Don’t Work

Many business owners try workarounds — going cash-only, keeping a stricter register, calling customers personally. These help to some extent, but:

- You cannot realistically go fully cash-only without losing customers

- Maintaining a manual list is time-consuming and error-prone

- Personal calls are awkward and don’t scale as your customer base grows

The real solution is not more discipline — it is a smarter system that tracks credit automatically, sends reminders professionally, and gives you a real-time view of your outstanding balance at all times.

5. Old Credit Is Practically Written Off

When records aren’t maintained properly, outstanding amounts older than 3 to 4 months are essentially lost money. Both you and the customer forget. It silently becomes a business loss — one that never shows up in your books, but always shows up in your stress.

This Is Not Just Your Problem

India has over 6 crore registered small businesses, and the MSME sector consistently shows that 15 to 25 per cent of a small retailer’s revenue is tied up in outstanding credit at any given time.

That means if your monthly sales are ₹1 lakh, between ₹15,000 and ₹25,000 is always sitting outside your business — in someone else’s pocket.

This is not a personal failure. It is a systemic problem that affects millions of small business owners across India who lack the right tools to manage it.

Why Traditional Solutions Don’t Work

Many business owners try workarounds — going cash-only, keeping a stricter register, calling customers personally. These help to some extent, but:

- You cannot realistically go fully cash-only without losing customers

- Maintaining a manual list is time-consuming and error-prone

- Personal calls are awkward and don’t scale as your customer base grows

The real solution is not more discipline — it is a smarter system that tracks credit automatically, sends reminders professionally, and gives you a real-time view of your outstanding balance at all times.